Elgin Audit Reveals Eight Material Weaknesses; Abbott Orders Texas Rangers to Investigate

Read the single audit report the City of Elgin didn't post online.

By Kristen Meriwether, Publisher

On Thursday, Texas Gov. Greg Abbott ordered the Texas Rangers to investigate the City of Elgin for potential violations of state law. They will investigate the city’s budgeting process and financial processes for violations of state law.

"There have been serious and potentially criminal accusations made against the City of Elgin that need to be investigated. Texans expect their elected officials to be honest stewards of taxpayer dollars and conduct the people's business openly, and in compliance with Texas law,” Abbott said in a press release Thursday. "Due to the accusations of chronic financial mismanagement, including inconsistent accounting practices and unreconciled bank accounts, in potential violation of multiple state laws, I directed the Texas Rangers to launch an investigation into the City of Elgin's finances to ensure transparency and full compliance with state law."

In response, the City of Elgin released the following statement Thursday afternoon: “The City of Elgin will cooperate fully with Governor Abbott’s recently announced investigation into the City’s finances. Recent audits conducted by an independent auditing firm for fiscal years 2022 and 2023 found no evidence of wrongdoing or criminal activity and no missing funds. Any issues discovered in the audits concerning accounting procedures are being addressed with current staff. All audits for the City can be found on the City's website, elgintexas.gov.”

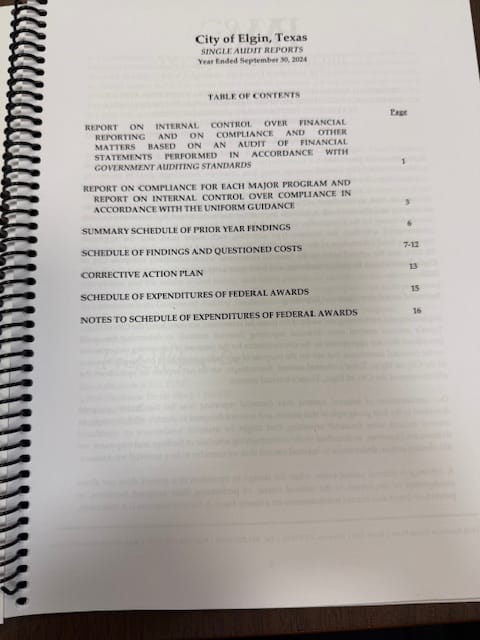

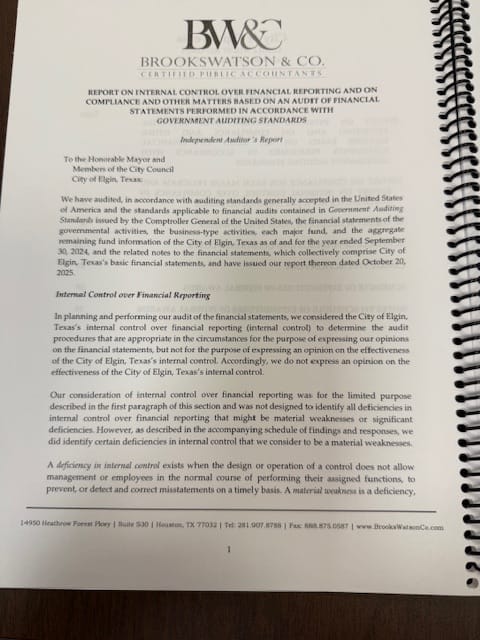

While the audits are online, the City of Elgin was given a supplementary single audit report with their annual financial audit for the year ending Sept. 30, 2024. This report, dated Oct. 20, 2025, was not made available online with the financial audit, but is available at Elgin City Hall by requesting to view the audit. Smithville Texas News viewed that record on Tuesday and we have included photographed pages of that report at the end of this article so the public can access it online.

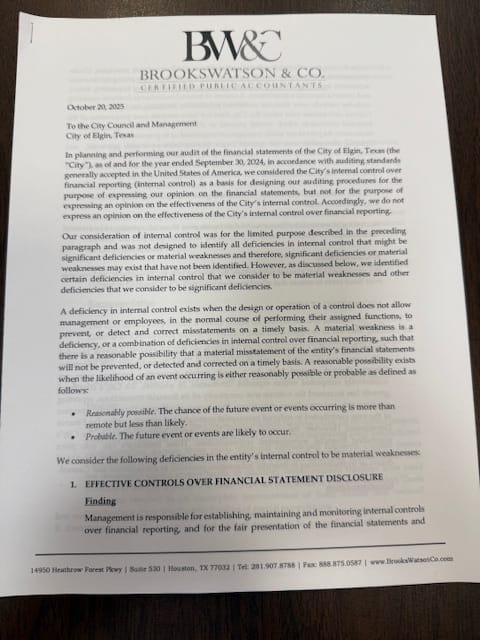

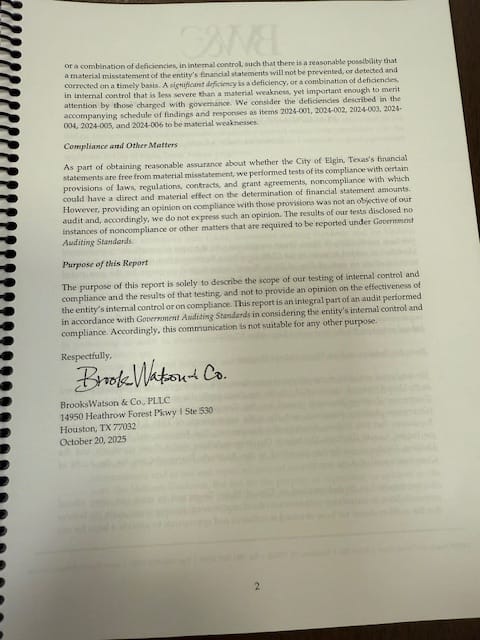

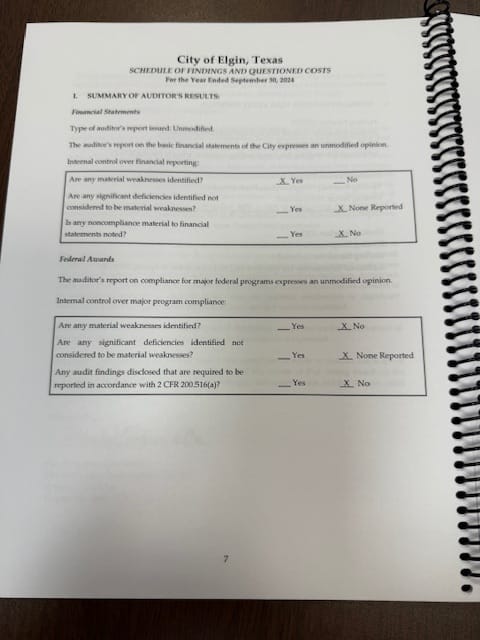

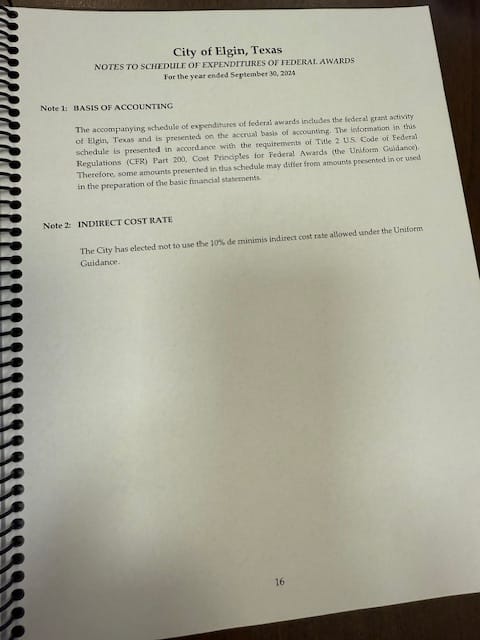

In this supplemental report, the auditor, BrooksWatson and Company, listed eight material weaknesses in the city’s internal controls.

A material weakness is, “a deficiency, or a combination of deficiencies in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected on a timely basis,” according to the letter.

The following were considered, “deficiencies in the entity’s [City of Elgin] internal control to be material weaknesses.”

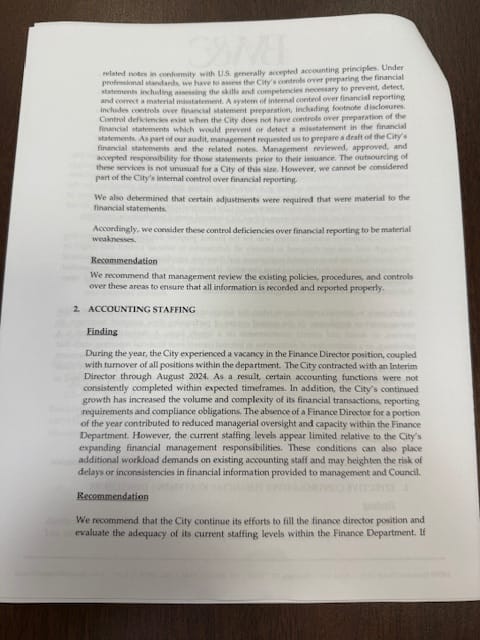

1. Effective Controls Over Financial Statement Disclosure

The auditor noted that the City of Elgin requested they prepare a draft of the city’s financial statements and related notes, which were then reviewed and approved by the city.

The report noted that while it’s not unusual for a city of Elgin’s size to use a third party company, the auditor said, “we cannot be considered part of the city’s internal control over financial reporting.”

The report also noted the auditors had to make adjustments to the financial statements.

Auditor's Recommendation: “We recommend that management review the existing policies, procedures and controls over these areas to ensure that all information is recorded and reported properly.”

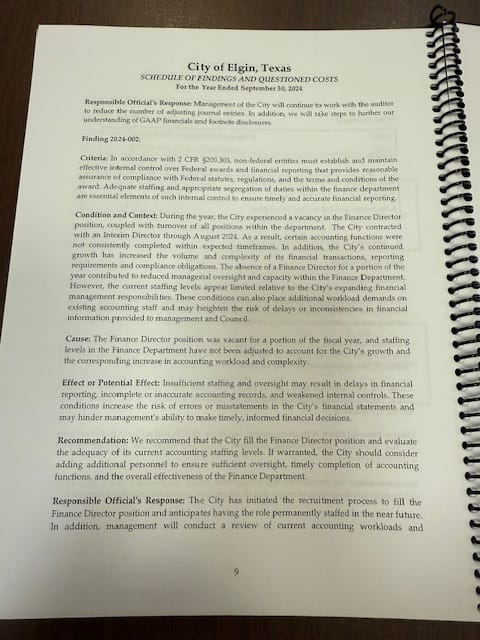

2. Accounting Staff

The letter noted that for fiscal year 2024 the City of Elgin did not have a director of finance and all positions in the department had turned over. Exact numbers of staff who left and dates of those departures were not provided. An interim finance director filled the role through August 2025.

Smithville Texas News reached out to the City of Elgin to confirm a timeline of finance directors hire and departure dates. Since it involved personnel, we were instructed to file an open records request.

Public records show Pamela Sanders, who is the city’s human resources director, is currently acting as the finance director.

Public records show Belen Peña signing investment reports in late 2022 and again in September 2023. By May 2024 she was listed as the finance director on a bond document as the finance director for the City of Manor.

Charles Cunningham was the next name we found that served as finance director prior to Peña. Public records show him listed to give a presentation to the EDC on Jan. 16, 2018, and the last document we found was in June 2021 where his email was listed as a contact for the five-year capital improvement plan.

In February of this year Cunningham and his wife were involved in a murder-suicide at their home.

The auditor’s letter also said the city’s growth has increased both the volume and complexity of the financial transactions, noting the current staffing levels “appear limited relative to the city’s expanding financial management responsibilities.”

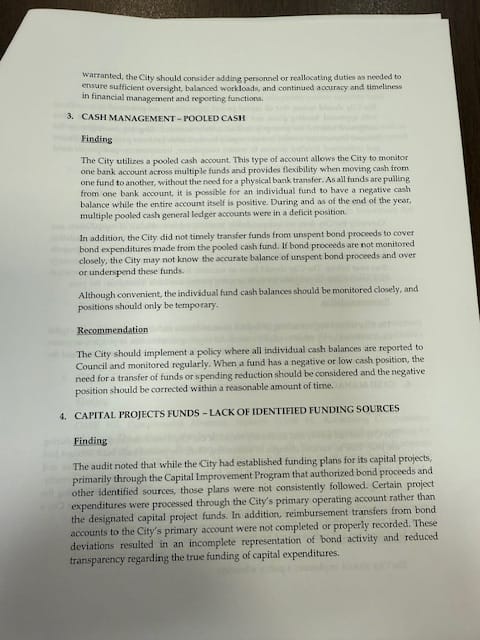

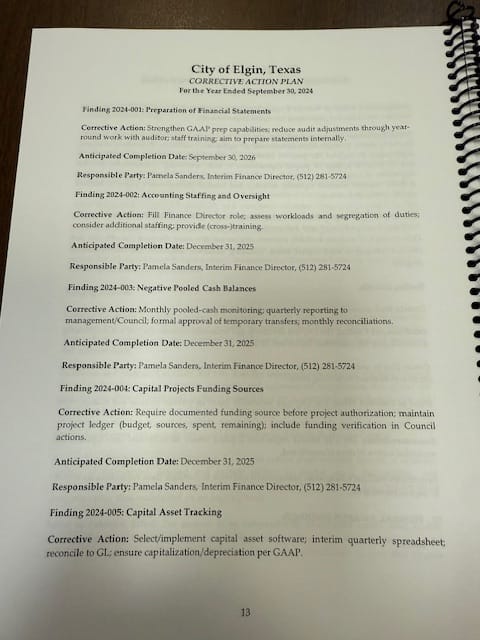

Auditor's Recommendation: “We recommend that the city continues its efforts to fill the finance director position and evaluate the adequacy of its current staffing levels within the Finance Department. If warranted, the city should consider adding personnel or reallocating duties as needed to ensure sufficient oversight, balanced workloads, and continued accuracy and timelines in financial management and reporting functions.”

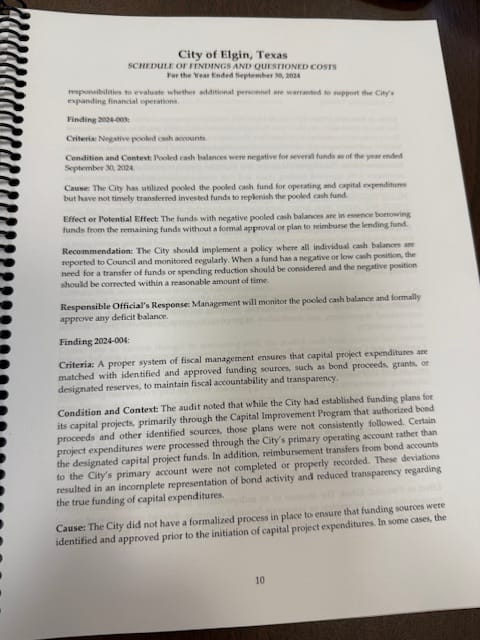

3. Cash Management–Pooled Cash

The City of Elgin used a pooled cash account, meaning multiple funds were in one bank account. This allowed the easy transfer of money between funds without the need for a physical bank transfer. The downside to using this method is that funds can go negative but the account is positive.

The letter notes during this fiscal year multiple pooled cash general ledger accounts were in a deficit.

The letter added that the city did not transfer unspent bond proceeds to cover bond expenditures made from the pooled cash account.

Auditor's Recommendation: “The city should implement a policy where all individual cash balances are reported to council and monitored regularly. When a fund has a negative or low cash position, the need for a transfer or funds or spending reduction should be considered and the negative position should be corrected within a reasonable amount of time.”

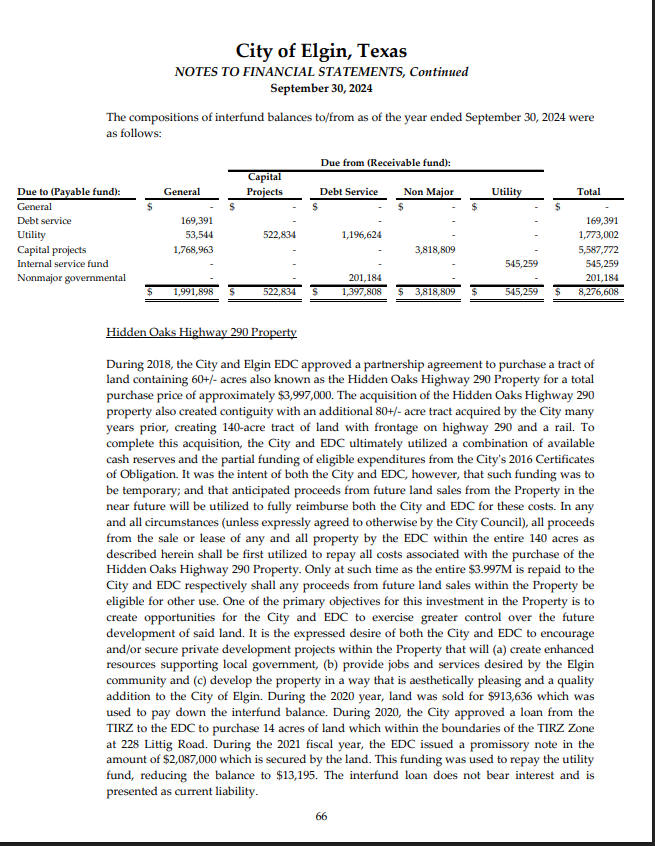

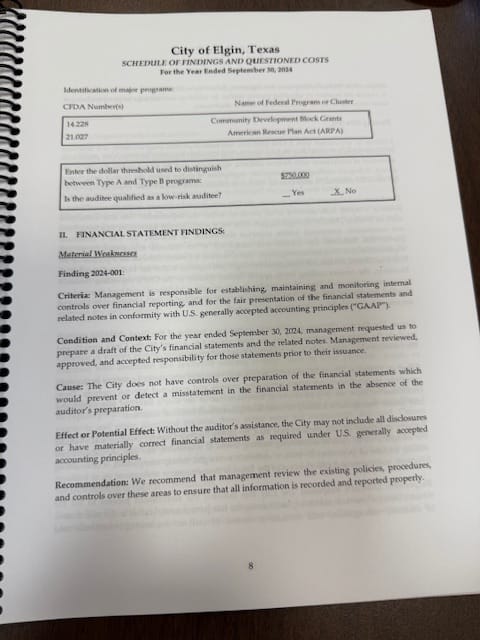

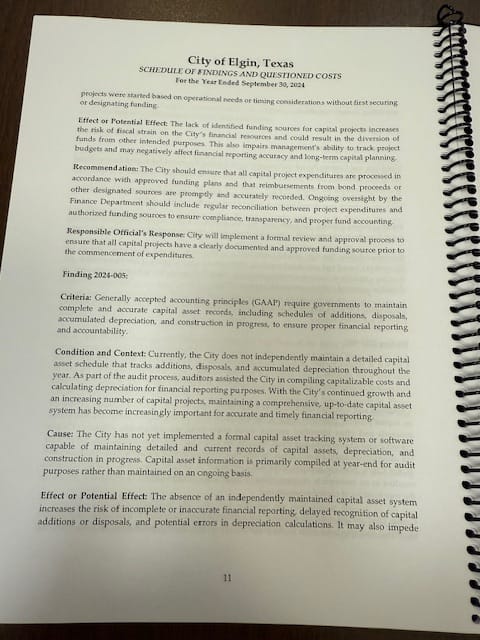

4. Capital Projects Funds–Lack of Identified Funding Sources

The letter noted that certain capital project expenditures were processed through the city’s primary operating account instead of in a designated capital project fund. Neither the letter or the supplementary report identified which capital project or expenses had the issues, or the dollar amounts of those issues.

But page 66 of the financial audit provides financial statements and a narrative for the Hidden Oaks Highway 290 Property project. The auditors noted how many times money was loaned between the City of Elgin, Elgin’s Economic Development Corporation, and Elgin’s TIRZ.

Additionally, the letter noted reimbursement transfers from bond accounts to the city’s primary account were not completed or recorded correctly. “These deviations resulted in an incomplete representation of bond activity and reduced transparency regarding the true funding of capital expenditures,” the letter said.

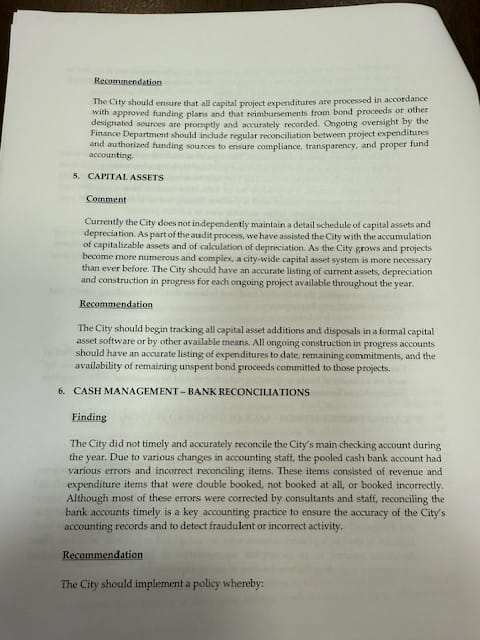

Auditor's Recommendation: “The City should ensure that all capital project expenditures are processed in accordance with approved funding plans and that reimbursements from bond proceeds or other designated sources are promptly and accurately recorded. Ongoing oversight by the Finance Department should include regular reconciliation between project expenditures and authorized funding sources to ensure compliance, transparency, and proper fund accounting.”

5. Capital Assets

The report said the City of Elgin does not independently maintain a detailed schedule of capital assets and depreciation, which has been required by the Governmental Accounting Standards Board (GASB) since 1999.

It is unclear from the letter if the city has never maintained the schedule, just didn’t do it for this fiscal year, or was out of compliance under a specific finance director.

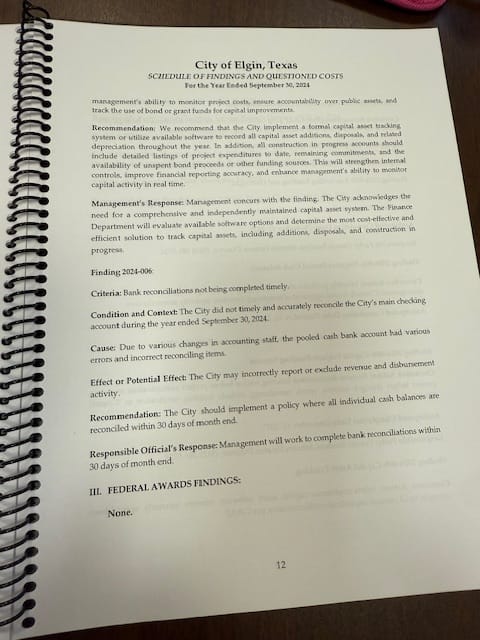

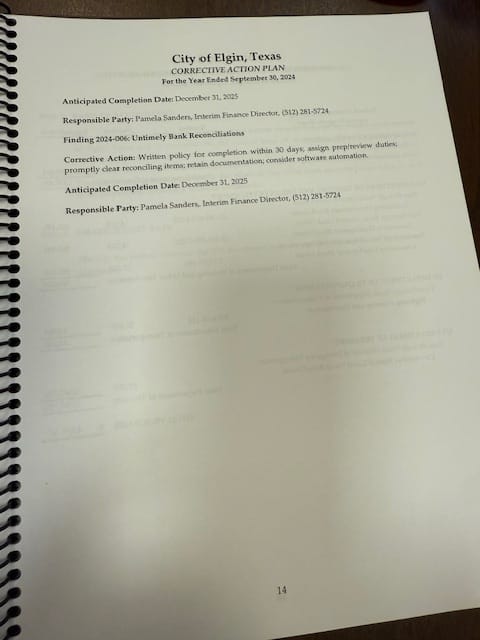

Auditor's Recommendation: “The City should begin tracking all capital asset additions and disposals in a formal capital asset software or by other available means. All ongoing construction in progress accounts should have an accurate listing of expenditures to date, remaining commitments, and the availability of remaining unspent bond proceeds committed to those projects.”

6. Cash Management - Bank Reconciliations

During fiscal year 2024 the City of Elgin did not accurately or timely reconcile the city’s main checking account due to staffing changes, according to the letter.

The accuracy issues included revenue and expenditures that were either double-booked, booked incorrectly, or not booked at all. The letter noted a consultant and the auditor corrected most of the errors.

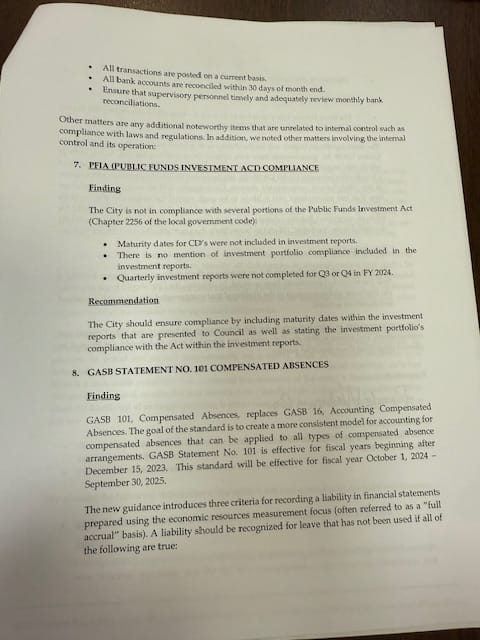

Auditor's Recommendation:“The City should implement a policy whereby:

*All transactions are posted on a current basis.

*All bank accounts are reconciled within 30 days of month end.

*Ensure that supervisory personnel timely and adequately review monthly bank reconciliations.

7. Public Funds Investment Act (PFIA) Compliance

Under Texas Government Code 2256, municipalities are required to follow numerous reporting requirements for investing public money.

The letter noted the City of Elgin did not have maturity dates for CDs included in investment reports, no mention of investment portfolio compliance in the investment reports, and no reports for the third and fourth quarter of fiscal year 2024.

Auditor's Recommendation: The City should ensure compliance by including maturity dates within the investment reports that are presented to Council as well as stating the investment portfolio's compliance with the Act within the investment reports.

8. GASB Statement No. 101 Compensated Absences

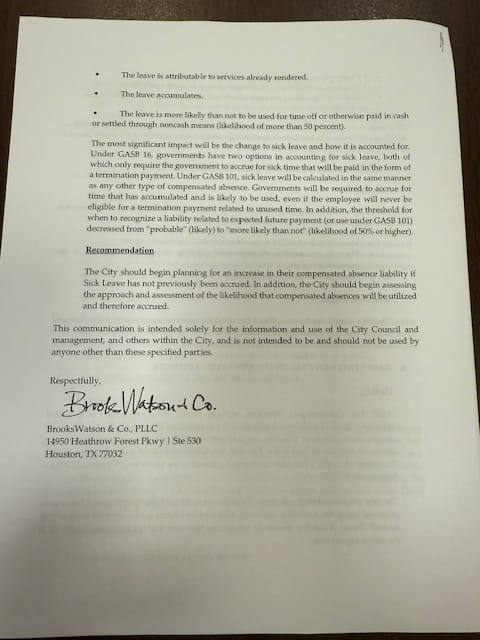

In 2023 GASB updated their standard for accounting for compensated absences and a significant change was made to how sick leave is accounted for.

The old rule only required governments to accrue sick time to be paid in the form of a termination payment. The new rule requires governments to calculate sick leave like any other leave, which allows employees to accrue the time.

The City of Elgin had not updated to the new rule, according to the auditor.

Auditor's Recommendation: “The City should begin planning for an increase in their compensated absence liability if Sick Leave has not previously been accrued. In addition, the City should begin assessing the approach and assessment of the likelihood that compensated absences will be utilized and therefore accrued.”

The Elgin City Council is expected to hold a special meeting on Wednesday, Nov. 5 to discuss the audit and audit findings. This meeting was scheduled prior to the governor's announcement today.

The meeting comes on the heels of a weekend clip from an Oct. 21 Elgin City Council meeting that went viral. The clip showed Elgin Mayor Theresa McShan telling Council Member Tiffany St. Pierre that she preferred to look forward instead of have a forensic audit look back.

"I'd love to know what happened, too. But I wasn't on the council then, nor was I mayor. We're not going to go back and try to figure out what all did happen while we're still spinning our wheels and not going forward," McShane said at the meeting.

After an exchange with St. Pierre, McShane continued, "I'm saying I don't want to spend months and years looking back. I want to go forward."

St. Pierre replied, "That's you. I want to spend months and years to go back. I want to know what my tax dollars were and my constituents want to know."

On Tuesday the City issued this statement regarding the hearing:

“We recommend that the public get acquainted with the facts prior to posting or reposting information on social media. The City of Elgin recently conducted an audit of the City's finances for fiscal year 2023. The audit was presented to City Council in an open meeting on October 21, 2025. The discussion from the meeting and the audit are both posted on the City's website, elgintexas.gov.

There have been no issues reported regarding the City's current finances, the City continues to build its reserves, and any issues discovered in the audit concerning accounting procedures are being addressed with current staff.”

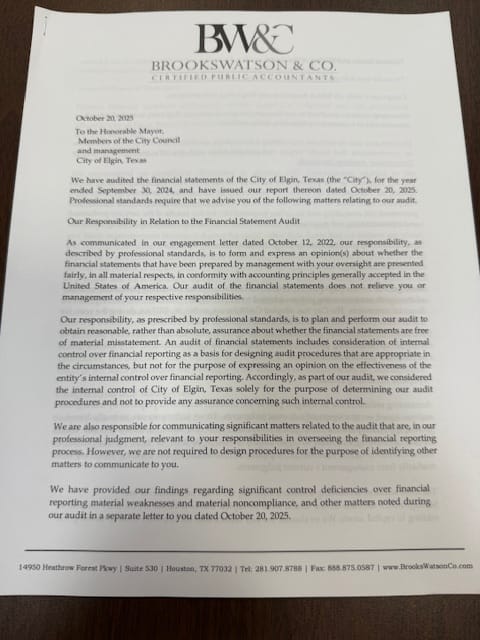

Letter 1

Images of letter from an auditor to the City of Elgin dated Oct. 20, 2025 regarding a single audit report on fiscal year 2024. The report was obtained by requesting to view the audit report at Elgin City Hall on Oct. 28, 2025.

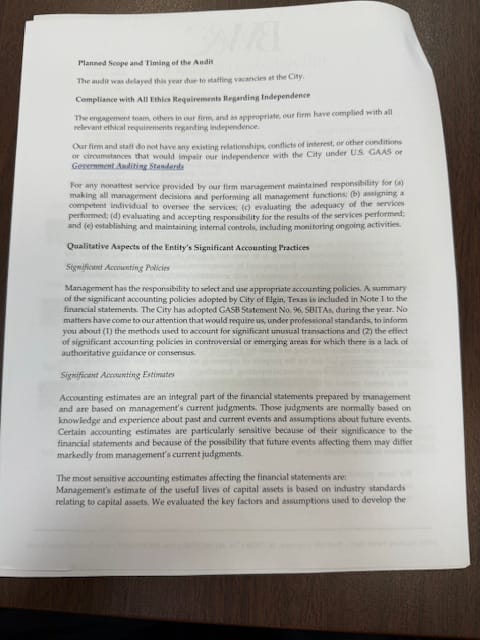

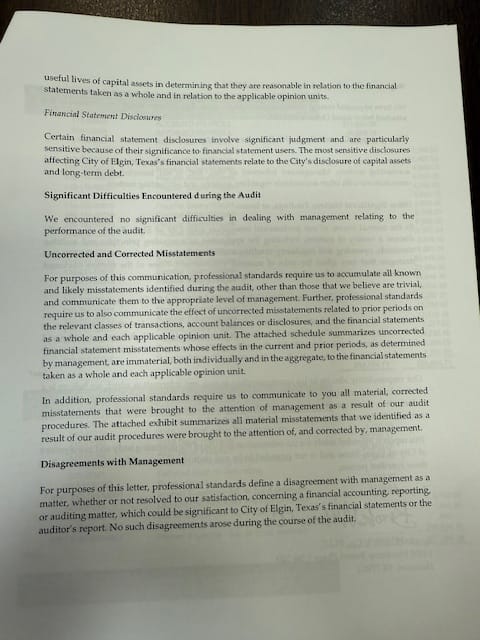

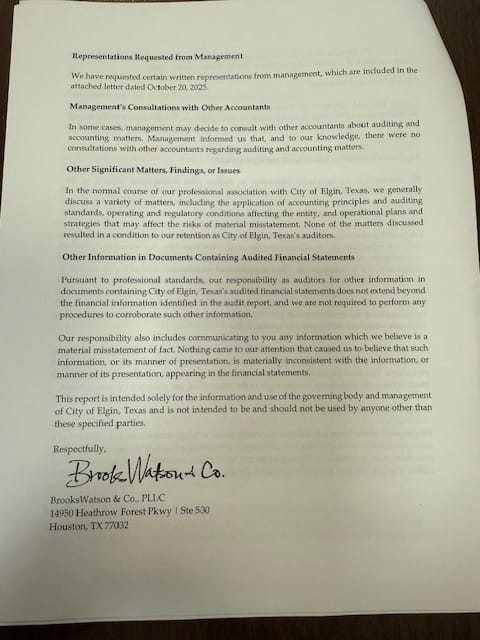

Letter 2

Images of a second letter from an auditor to the City of Elgin dated Oct. 20, 2025 regarding a single audit report on fiscal year 2024. The report was obtained by requesting to view the audit report at Elgin City Hall on Oct. 28, 2025.

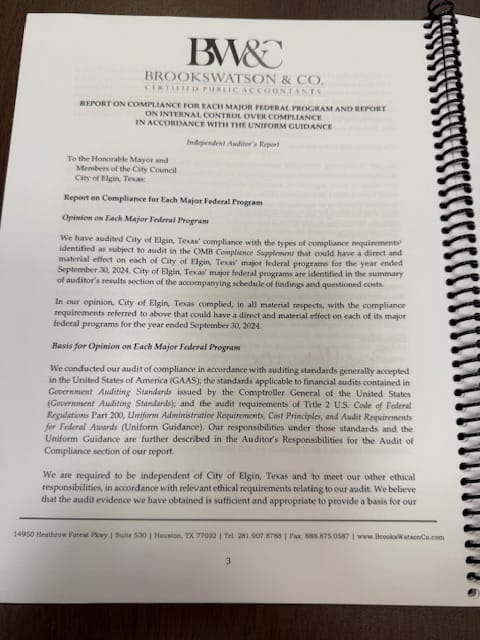

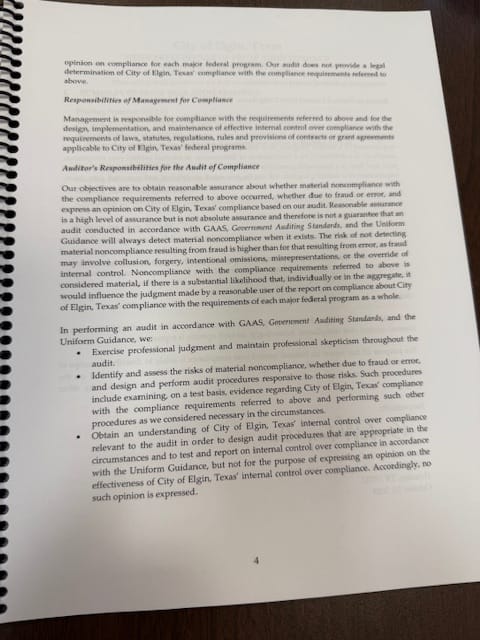

Single Audit Report (1 of 2)

Images of the single audit report on fiscal year 2024. The report was obtained by requesting to view the audit report at Elgin City Hall on Oct. 28, 2025.

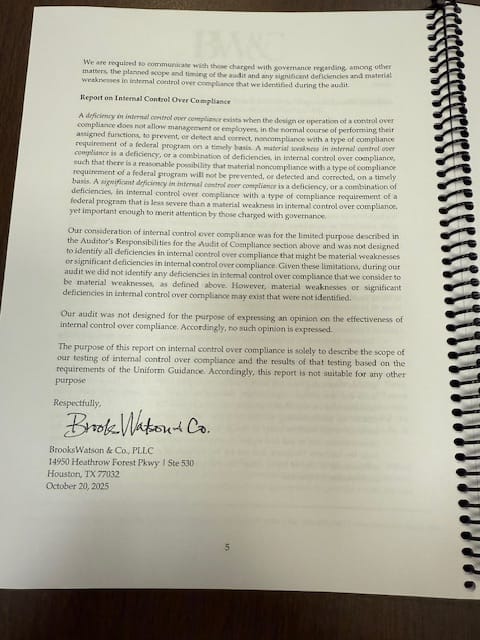

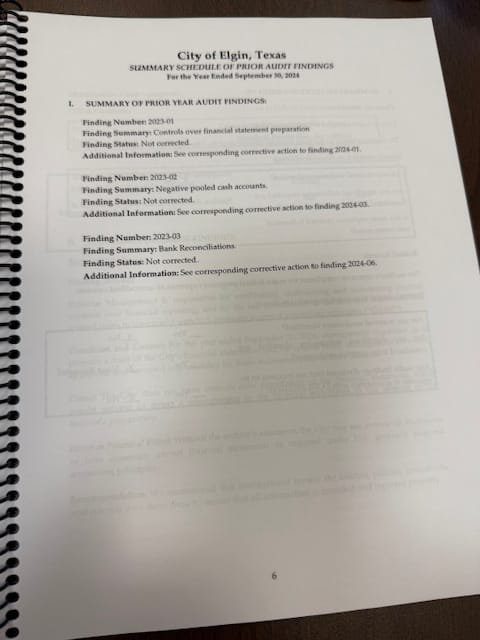

Single Audit Report (2of 2)

Images of the single audit report on fiscal year 2024. The report was obtained by requesting to view the audit report at Elgin City Hall on Oct. 28, 2025.

Comments ()